Owning Invisible Objects, Part 2

The second part of my first experience with fractional ownership of collectibles

Photo by Raul Valverde, Empty Art Galleries, 2010

If you stop for a moment you can hear the subtle smolder of money burning a hole in my pocket. In a way, I felt financially volcanic as I dropped a $500 minimum investment on 25 shares of a Yayoi Kusama painting from 1967. Do I really have the coin to gamble on this experiment? I keep a “profit” account where I set aside a tiny percentage of everything I earn, and, from that account, I mined the resources for this experiment. This means a smaller “bonus” this year but hopefully some sort of “windfall” in the sometime future. I estimate that the worst case loss of 500 bones will not destroy me, and, by any calculation, a total loss cannot happen. In most cases, it will go up, and I will feel exonerated for reducing my bonus in favor of a longer term gain. Or, I might feel worse about myself for profiting off the back of the commoditization of the work of an eccentric Japanese artist whose further fetishized work’s profits she will not directly experience. Look, I am trying to remain impartial.

In a way, the fact that the fractionalization of a tangible object into a jigsaw of intangible shares with the alleged intention of “democratizing” access to art investment indirectly demonstrates how messed up these markets are to begin with. That we even need to democratize it in the first place (do we need to democratize it? That is another debate.) suggests that markets for a small percentage of art and artifacts have metastasized within a feedback loop of investment and value/brand-building that feed off of each other to escalate prices and gains alike. And, it works for those that can participate. I will not claim to understand any nuance of these markets and games and will stop short of further interpreting or speculating about any aspect of them. I merely want to make the point that if we intend to invest in works in these markets, that an institution made for investing created that opportunity. Masterworks has created similar opportunities but, instead of offering a menu of entrees, they provide the option to purchase as little as a bite of each dish in order to allow the less fortunate to eat at least something.

Investments, however, do not care about my cuddly, sensitive feelings and emotions regarding artist intent and historical context. They care about my money. They receive their money when I receive mine. Their will pocket 20% of the money I make when they sell the work plus 1.5% equity a year as a non-cash management fee. So, at least we have aligned interests.

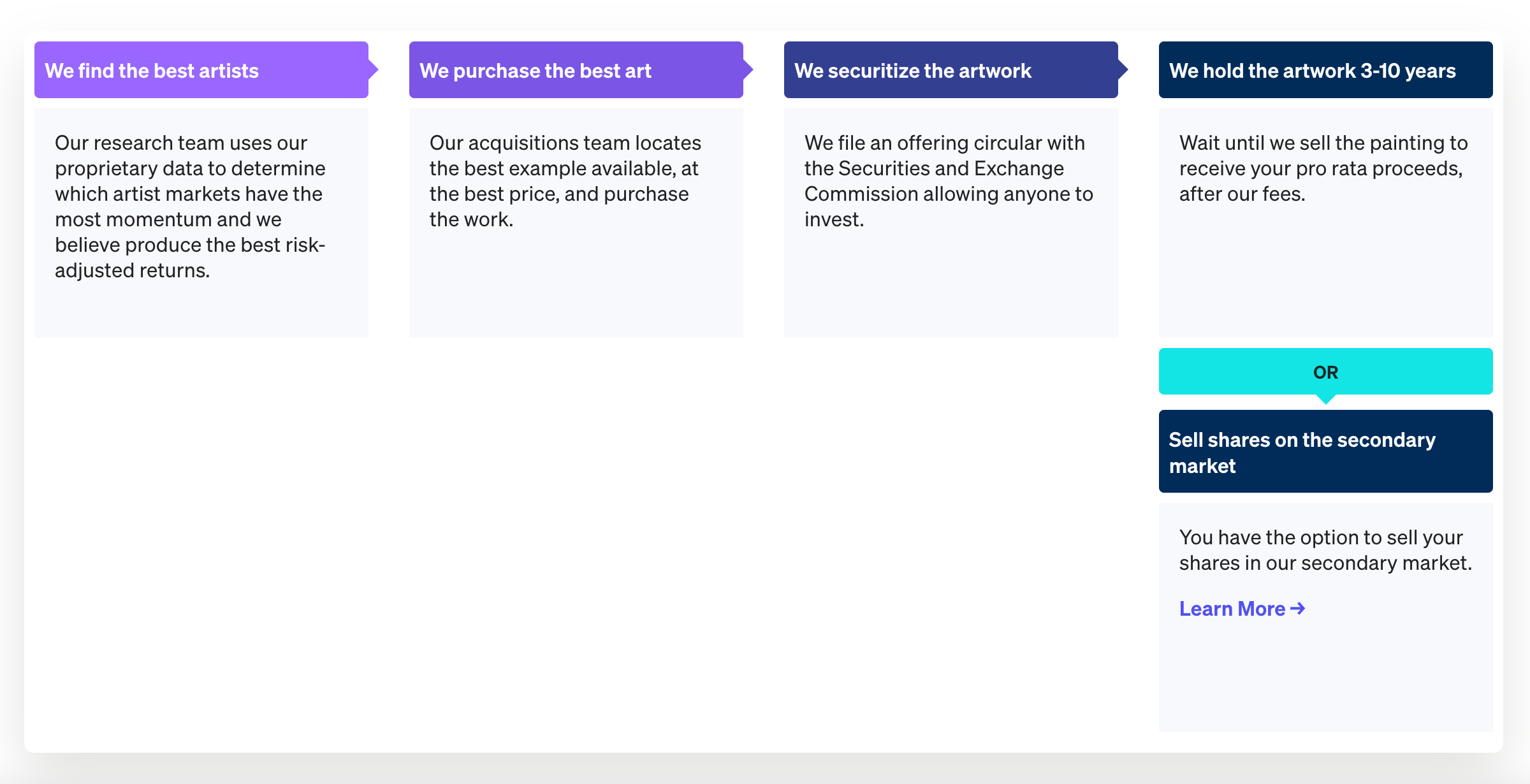

With that in mind, I want to discuss the basic operations of Masterworks. If you want all the intricate details, go to their website, but suffice to say, they get judged on whether they make money for their clients. And, their clients do not need to care about the work or its intent. See the basic process below.

Masterworks declares, to my earlier point:

According to Artprice, blue-chip art has outperformed the S&P 500 by 180% from 2000–2018. Deloitte estimates the total value of art to be $1.7 trillion. For the first time, you can invest in this exciting asset class.

This shakes out in interesting ways. First, they actually purchase the pricey, mainstream-y works based on their own asset appreciation criteria and then, because the business involves asset trading, they have to abide by Security and Exchange Commission (SEC) regulations. I find it interesting that their circular revealed that each work offered for sale is its own independent company. Think of it in this over-simplified, somewhat naive way, if you buy a 5-unit apartment building for $1m and then sell each apartment for $400,000 you make $2m. In the case of Masterworks, the value will ideally appreciate whilst in their custody so that by the time they sell their “apartments” they will each sell for more than $400,000. We also do not know what they paid for the building.

While in the possession of Masterworks, the pieces get stored somewhere and you probably will not get access to the physical object, though they do not completely shut down that option, however. I will try to get access to see my investment for the next part of this series.

Knowing what I know about this process, I initiated it by connecting my bank account to their system. Like connecting to PayPal, it takes a few days to set it up because they transfer a small amount of money into your bank account to verify its legitimacy. Once connected, I assessed my odds based on a list of offerings of mostly modern and contemporary art. Jean-Michel Basquiat, Yayoi Kusama, Joan Mitchell, Sam Gilliam, Carmen Herrera, Kazuo Shiraga, and Agnes Martin represent some current options. In the past, they apparently dabbled in a Monet, but that one work outlies the majority of their dealings which primarily stem from the late Gen X-y 1980s to the Gen Z-y present.

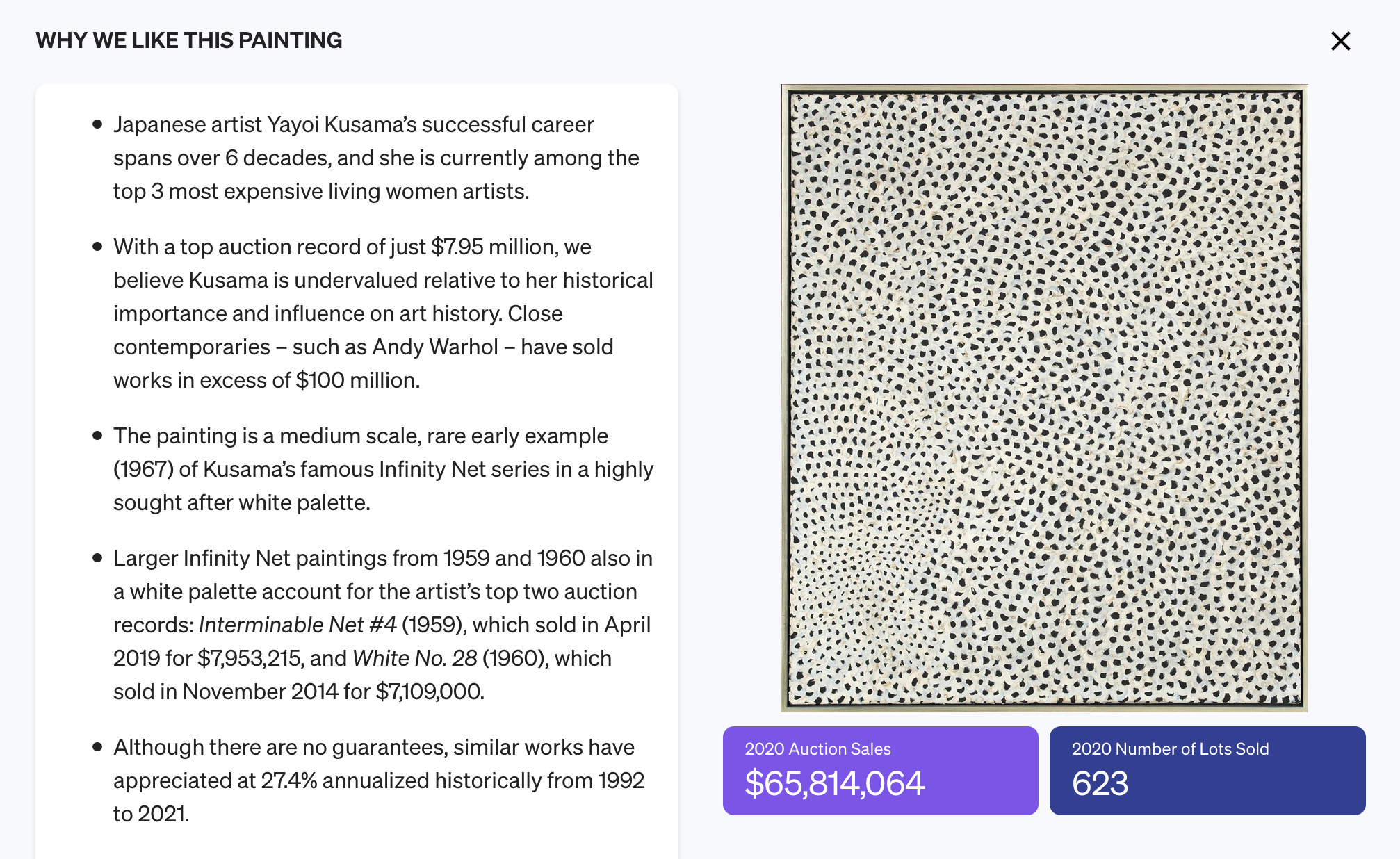

With each offering, they provide an investment thesis and historical appreciation rates. In the case of the Kusama work that caught my attention, they note the price appreciation at 27.4%, one of the highest in the current offerings. They calculate the rate based on comps from historical sales. I chose that one because it is the the highest rate of appreciation plus I know the artist remains a hot commodity. The value seems extremely unlikely to diminish as long as that Infinity Room stays on exhibition.

The investment thesis explains the context in which they have judged it a good investment. I have included a screenshot of part of it below. I reckon the fact that they have bet on it to the point of purchasing the work shows some confidence in their due diligence.

So, as I anticipated, the investment considerations do not talk about the content or context of the object. They highlight the fact that this “Infinity Net” series is highly sought after but not more. Perhaps this is the investment equivalent of not naming your farm animals: when they go off to slaughter or get sold, you feel less attached and, consequently, less distraught.

As you already know, I placed all of my meager chips on Kusama like a kid in Vegas and am waiting for the investment to go through. Several days have lumbered by and I still do not have my 25 shares listed in my portfolio (their term). They apparently only appear after the offering has closed – meaning, I believe, that they have sold all the shares in the work. I do not know how long I will have to wait for this to happen. And then, we wait… for years.

Alternatively, if I do not wish to wait the projected 3–10 years to sell, I can sell my shares on their secondary market. That is a nifty option that I may have to later explore. For now, however, I will watch for the offering to close like eying the final straggling passengers boarding a full plane, with disdain for not arriving sooner because I am anxious to take off.

I welcome your thoughts and questions below.